XI. German Austerity and the Ordo-liberals.

Unfortunately for Cyprus the obfuscation and delays of the Christofias presidency had placed the negotiation of the bailout smack bang in the middle of the German political cycle.

The SPD and Greens, seeking a wedge issue to differentiate itself from Merkel’s CDU, did an about turn on its criticism of the meanness of previous bailouts and decided to aggressively campaign for more stringent bailouts. According to the FT,

Both SPD and Greens declared that Cyprus must abandon its current “business model” of providing a tax haven for wealthy Russian depositors in particular, before they would approve any rescue. (FT Quentin Peel 18th March 2013)

This change of policy six months away from the German elections has been disastrous for Cyprus and has led to a competition to see who can impose the toughest conditions and rhetoric on Cyprus in German politics and in the media. Such electioneering and the emergence of an anti-European party in Germany has,

‘reinforced a deep-seated national conviction that moral hazard must be avoided by forcing private investors to share the costs of failure with taxpayers.’(FT Quentin Peel 18th March 2013)

This is a position reflected in Wolfgang Muchau's recent comment that ,

'It is fair to conclude that a change in government will not change Germany’s euro policies – in that sense the German elections will have few consequences for the eurozone rescue policies'. (at eurointelligence).

The orthodoxy of austerity and budgetary rectitude is hardening across Europe - in Germany, the Netherlands, the UK, and within the IMF. The shift in position of the SPD and Greens may be tactical but it remains to be seen if they can reverse that position after the elections. It is also noticeable in the UK how attitudes against the poor and redistribution are hardening.

Cyprus has undoubtedly been treated harshly but this may be more a sign of a general hardening of positions in Germany, the IMF, the Netherlands, the emergence of a stronger coalition of 'haircutters' (the 'High Priest' in the IMF, the German and Dutch finance ministries, Brazilian concern over 'soft' loans to EU members etc- see below) and the weakness of oppositional voices and narratives within the EU and EC rather than a particular determination to 'get' Cyprus - although size clearly does matter in these things.

The Ordo-liberal hegemony in German economic thought and practice

Great article in the FT (20 September 2011) about the roots of German economic orthodoxy by Ralph Atkins back in 2011

Europe’s experience of fascism and communism encouraged postwar Germans to limit discretionary government action. As such, ordo-liberals are akin to free-market economists in the US and elsewhere. But they kept markets within tight rules – hence the country’s image as over regulated. The concept of Ordnungspolitik – the practical application of ordo-liberalism – was combined with the idea of a Soziale Marktwirtschaft, an economy requiring income redistribution and generous welfare safety nets.

Berlin’s Ordnungspolitik conscience lies in the economics ministry and in the Bundesbank. The latter created to enforce anti-inflationary policies after the disasters of the interwar years.

Today’s fear is that the ECB’s large-scale government bond purchases are akin to the Reichsbank running the printing presses during the Weimar Republic.

and

Leading conservative economists argue, however, that the problem is not that rules proved worthless [in the Eurozone crisis] – but that there were not enough of them.

In contrast to the IMF and ECB which believe in austerity and discipline but employ it with pragmatism and a mix of sticks and carrots

German conservatives couple economic arguments with a moral conviction that, if rules are to work, inappropriate behaviour should be punished whatever the impact on other countries.

European monetary union allowed Germany to pursue a model based on export driven growth based on its increasingly competitive industrial sector. And the rest of Europe could not keep up through devaluation as had happened in the past. But, says Heiner Flassbeck, a former state secretary in the finance ministry and critic of conservative economists,

"The small problem with that is that the others [members of the Eurozone] are now bankrupt... Mr Schäuble does not understand the argument that a government cannot behave like a Swabian housewife."

There is little sign that the ordo-liberals are about to be cast out from their policy castles. They dominate Germany's universities and 'full-blooded pro-stimulus Keynesians are rare'.

Good background article in NYT Stewart 15 June 2012 on German fiscal rectitude

Jacob Kirkegaard, an economist and European specialist at the Peterson Institute for International Economics, ... ascribed Germany’s stance to a combination of character, politics and economics ... Many Germans “are like the Swabian housewife,” [says] Peter Bofinger, a German economist and member of the German Council of Economic Experts “If you’re spending too much, then you have to stop, and it’s better to stop now than tomorrow,” he said.

European Wealth and Incomes and Germany

'the typical German household is three times less wealthy than its Spanish or Italian counterpart, according to a Bundesbank study of personal wealth that was published this week. Whereas the median Spanish household has net wealth of €178,000, the equivalent in Germany is €51,000.'

This difference is largely due to the low rate of home ownership in Germany (44 per cent) comparede to say, for example, Spain at 80 per cent.

The Bundesbank study also showed that many Germans rely on the country’s relatively strong social provision and safety nets than on theri accumulated wealth and at least in part due to this Germans had fewer reasons to save than many Europeans (see FT Wilson 22 March 2013).

Lower incomes than Cyprus

Another way of looking at relative levels of affluence is through mean and median income equivalised disposable incomes. Amazingly the table below shows that Cyprus had higher median equivalised disposable incomes in all three age brackets (18-24, 24-49, and 50-64) than Germany in 2007 (see Economic Fallout.

The median equivalised income in Cyprus in 2007 was €18,230 compared to €11,577 in Greece and €17,338 in Germany.

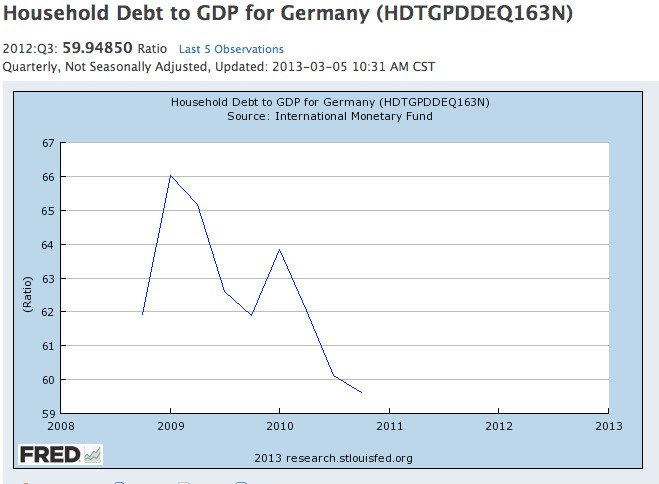

Household debt in Germany

See the graphic below from the St Louis Fed 2013 from IMF 2011 where

The data for household debt comprise debt incurred by resident households of the economy only. This Financial Stability Inidicator measures the overall level of household indebtedness (commonly related to consumer loans and mortgages) as a share of GDP.

Household debt in Germany fell from 66% to 60% between 2009 and 2011.

Compare this to Cypurs's household debt of 140% of GDP for2007.

Without wanting to labour the point these differences in accumulated wealth, social provision and equivalised income maybe do have something to do with the national psyche and the appeal of the message from the ordo-liberals regarding the need to 'live like a Swabian housewife' - that is debt-free and with a balanced budget.

Germans live on relatively low incomes (need to look into this further) with little accumulated wealth or savings to fall back on. Social provision from the state is their backstop in hard times but there is little room for error in budgetting and getting by.

I remember reading with surprise that Germany is a much less urbanised country than some members of the EU. And although there are the big industiral giants the family firms - the Mittelstand - are a crucial component of Germany's export-led economic success.

BND Secret service checks up on oligarchs

On 5 November 2012 Speigel's english online edition reports that the German secret service, the BND (Bundesnachrichtendienst), have released a report into Russian money and money laundering in Cyprus. It claims €26bn of Russian money is deposited in Cypriot banks.

German parliament set to approve Cyprus aid

Today the German parliament wil approve the EU ESM funding to Cyprus.

The position of the SPD has been particularly interesting. According to the FT Ehrlich 16 April 2013

'The SPD this year considered voting against Cypriot rescue, seeing it as a chance to inflict a damaging defeat on Ms Merkel in advance of September’s elections.'

It appears that the SPD had a direct and unfortunate impact on the harshness of the bailout - or bail-in as it became. The Green party were involved in this too.

Said Carsten Schneider, SPD budget spokesman, “The bail-in (of some creditors and depositors) was a game changer ...without that, an approval would have been impossible for us.” Mr Schneider said the bail-in was a “template for the future banking union.”

If the SPD holds to this line, and is now being preicted the next German government is formed of a grand coalition of the CDU and SPD its appears unlikely that future bailouts will become easier.

The German Model

Controversy has raged over the relative household and per capita wealth/income of Germans and Cypriots (see Economic Fallout).

It does appear that real median incomes in 2010 in Cyprus and Germany were broadly equal. When equivalised at purchasing power standards median Cypriot incomes are considerably higher than those in Germany.

With regard to household wealth German households have much less wealth than Cypriot households, even when adjusted for household size. This is to some extent accounted for by the greater prevalence of home ownership in Cyprus and the rapid rise of property prices on the island. In contract house prices have been slow to rise in Germany - partly at an aggregated level due to reunification and depressed prices in the former East Germany. It has also been argued that the strict control of rents in Germany makes rental a more attractive option than in other parts of Europe.

Finally, one needs to consider the wealth of Germans in terms of their access to public welfare goods and the accumulated wealth in pension funds.

Even when all this is taken into account the position of Cypriot households vis a vis their German counterparts is striking, and very different from that of other Southern European EU member state households.

Of course this kind of statistical analysis and its findings are anathema to Cypriots and manna to the right wing and populist press in Germany and getting to the bottom of the issue is difficult.

It would be able to plot growth, household wealth and indebtedness and median incomes in Germany and Cyprus over the period 1960-2013.

In the last decade growth in Cyprus has been very dynamic - at over 3 per cent a year whilst in Germany the economy has struggled to grow at all. In the same period I would expect to see both a rapid rise in real wages and incomes in Cyprus whilst these indices have flatlined in Germany.

And with household wealth I would expect to see a rapid rise in Cyprus due to both the housing bubble and an increasing stock of saved wealth as Cypriots deprived of access to a reliable welfare system (particularly health) save on a precautionairy principle for healthcare and old age (elder poverty in Cyprus is the highest in the EU).

It is ironic that it is only in the last few years that the tables have turned with regard to Cyprus and Germany. Structural reforms and years of wage restraint are now helping to fuel export-led growth despite the strength of the euro. Add to this the lessening burden of reunification costs - transfers from West to East stacked up to an impressive 1.3 trillion euros (Reuters).

At the same time the political balance in the EU has shifted and has propelled Germany, however reluctantly, into a position of political and economic dominance. Traditional checks on German power - for example France - are weakened and the UK has absented itself from the debate by both its position outside the euro and the ill-advised manoeuvres of the Cameron Conservative party in euro-groupings of the centre-right.

In parallel the deepening of the eurozone crisis has made it increasingly difficult for Germany to hide behind the bland collectivity of the European Commission as its national interests are threatened by the spectre of systemic crisis.

In its domestic politics Angela Merkel has carved out a position that has kept an increasingly sceptical German populace onside while extending 'solidarity for solidity' to eurozone economies in crisis. The forthcoming September 2013 elections have added a new dynamic to the ordo-liberal orthodoxies that inform German economic policy at home and within the eurozone. The u-turn performed by the SPD and the Greens from voices of constraint to cheerleaders of a more robust bail in of bank deposit and share/bond holders has removed one constraint and racheted up the rhetoric.

This has coincided with a hardening of the position of the International Monetary Fund and the reinvigoration of the influence of its high priests of budgetary rectitude and structural reform under the leadership of Christine Lagarde.

Couple to this the lessons that Europe at many different levels has been learning about both the depth of the crisis, the recklessness of bankers under the sway of cheap credit and mesmerising gains in personal wealth and prestige and the limits of domestic acceptance of bailout burdens in both the polities of those both extending and receiving a particular and changing confection of European solidarity.

Cyprus strolled into this toxic mix having tried everything to save it banks and public finances without recourse to the hand proferred by the European Commission (a massive and ruinous bet on Greek bonds using cheap ECB loans, a 2.5 billion euro loan from Russia, raids on its own state controlled industries to keep the cashflow positive, further appeals to Russia and missions to China).

And it brought with it a particularly toxic brand of offshore finance - the dominance of two banks locked in what looks like ego-driven and disastrous competition, massive exposure to Greek bad loans and sovereign bonds, a fragile reliance on deposits for liquidity and capitalisation that at the sniff of default were easily withdrawn from the system, and all the accusations of being a tax haven fuelled by Russian money using the island's light-touch regulatory regime to turn around vast flows of corporate and personal wealth -the single fact that stands out here is that until the bailout Cyprus was the largest source in the world of foreign direct investment into Russia.

By the time Cyprus's elections had run their course and the craven and self-deluded government of Demetris Christofias had been shunted into history the ECB, the European Commission and Germany had run out of patience with their distant south-eastern European outpost that had built up resentment and fury over its broken promises over a tacit peace-for-accession deal with regard to the continued division of the island and the Annan Plan.

Yes, the bailout and bail in process has been a catalogue of errors but portraying this as Germany giving a good and vindictive hiding to tiny Cyprus is a travesty of a dynamic and nuanced situation. Unfortunately the continued revelations that come out of Cyprus on a weekly basis - the accusations of forgiven loans to politicians, the massive withdrawals and transfers of money out the country on the eve of the bailout (that appear to involve the new President's family) and the Attorney General's instruction to drop a drunk driving without tax or MOT against his 32 year old son do nothing to dispel the image of a banking and governing elite mired in sleaze and corruption.

Of course Germany is no saint. Its regional banks have been in considerable trouble and it is no stranger to charges of corruption and wrongdoing in high places - the recent spate of plagiarism findings against PhDs in high places is a case in point. And Germany despite its ordo-liberal protestations has broken European financial rules when it has suited and who is to say that the modality of particular bailouts - for example with regard to the exposure of German banks to the Irish economy - has not benefitted particular German interests. But at the end of the day it is Germany that is bankrolling solidarity programmes in Spain, Portugal, Ireland, Greece and now Cyprus.

After ten years of tight family and state finances and high unemployment while much of Europe party-ed it is not surprising that Germans should feel a little pissed-off.

The increasing harshness of the rhetoric in Germany and Cyprus (and amongst the ranks of the Cyprophiles who just cannot get enough of identifying with the little island David's fight against the teutonic giant/EU bureaucrats/IMF monsters) bodes ill for the future.

The solidification of stereotypes and glib name-calling as analysis helps no-one (not even as cathartic venting) and reinforces mutual incomprehension and fury.

German domestic expansion and the amelioration of the economic imbalances that lie at the heart of the european project are widely recognised - from US Treasury Secretary Lew to a slew of well-informed economists and commentators - as the fastest way out of the mess we are in.

Overcoming the incomprehension and building some understanding of the different social and economic models that are a hallmark of the EU's continued diversity and richness is a task that vast army of journalists, researchers, bloggers and tweeters concerned with the fate of Cyprus and Europe could and should be applying themselves to.

The debate about money laundering in Cyprus rumbles on

The debate about money laundering in Cyprus rumbles on. On May 1st Haris Georgiades, the Cypriot Finance Minister, said that two money laundering audits - by Moneyval and Deloitte - had given Cyprus a clean bill of health. That's nice to hear but its a shame that the reports are not being published and we only have Georgiades' word on this.

The two best investigative articles on possible money laundering in Cyprus I have come across are in the FT and Wall Street Journal. Make up your own mind but for me there is enough smoke in both of these to suggest something akin to a fire.

Also the Moneyval report of 2011, whilst praising Nicosia’s international co-operation and its 'extensive measures to enhance its compliance with customer due-diligence reports” called for more standalone convictions, asset seizures and on-site supervisory inspections. It would be interesting to know if these were stepped-up post 2011.

Following the 2013 audits Georgiades said that "any remaining shortcomings, any ‘loopholes’ in the local AML system would be closed shut so that the subject of compliance is settled once and for all."

Georgiades went on to assert that allegations of money laundering against Cyprus were “a “staged affair, achieved through hyperbole."

Looking back over the accusations of money laundering and the 'hyperbole' to which Mr Georgiades refers it seems that the oft-cited villain of the piece is one Carsten Schneider, MP, and SPD budget spokesman who is quoted as saying said,

“We will not allow the money of German taxpayers to insure Russian black money deposits in Cypriot banks."

Schneider's comment was first reported in SpiegelOnline of 5 November 2012 where Schneider is quoted as saying,

"Before the SPD can approve loan assistance for Cyprus, the country's business model must be addressed," SPD budget expert Carsten Schneider said. "We can't use German taxpayers' money to guarantee deposits of illegal Russian money in Cypriot banks."

Note here the difference in the translation of Schneider's comment. In the FT the phrase 'Russian black money' is used. In Spiegel Online 'illegal Russian money' is used. In the German edition of Spiegel Schneider uses the word 'Schwarzgeld' which literally translated means 'black money'. But Schwarzgeld is (see Wiki De) a 'colloquial term for taxable, but untaxed income, which usually mainly from entrepreneurial or professional activity, so-called moonlighting [in]come'. (Machine translation).

In Spiegel Schneider made his comments in response to a German foreign intelligence agency (the Bundesnachrichtendienst - BND) secret report that, according to Spiegel Online,

'outlines who would be the main beneficiaries of the billions of euros of European taxpayers' money: Russian oligarchs, businessmen and mafiosi who have invested their illegal money in Cyprus.'

It also claims that,

'Money laundering is facilitated by generous provisions for rich Russians to gain Cypriot citizenship, according to the BND which found that some 80 oligarchs have gained access to the entire EU in this way.

According to the report the BND shared their findings with the troika: "The BND has analyzed the situation in Cyprus and then debated it with experts from the 'troika'."

All of which meant that, according to a member of Angela Merkel's government, "A rescue package for Cyprus could be very incendiary." And so it turned out to be.

Returning to Schneider's comments these were given greater potency by the addition of the adjective 'gleefully' by bloggers and later still by an article that suggested he had 'hooted' his comment. Schneider was also attributed with wanting to 'burn' Russian 'black money' when the original quote suggested he wanted was to avoid 'insuring' Russian black money.

The 'hooted' and 'burning' seems to be attributable to Joseph Cotterill at FT Alphaville. The 'gleefully' may come from a post by Satyajit Das on the Ritholz blog of 18 March that was republished in The Independent in an abridged version and in cross-posted in other blogs.

A small point but it is interesting how the rhetoric was ramped up by the addition of the words 'gleefully', 'hooted' and 'burn' by people who presumably were not there to hear Schneider's original comments.

Schneider had used the 'black money' comment before in September 2012 when he said,

“We in the SPD want people who have a lot of black money in Switzerland to pay taxes on that money.”

Germany on a different planet, claims Pew Research

There is an excellent across-EU opinion poll on changing member-state population attitudes by the Washington DC-based Pew Research. There is tremendous detail and I won't attempt to summarise it here.

Fred Kempe at Reuters has written a good summary that focuses on the decaying Franco-German relationship that has been the glue of the EU. He quotes the Pew Research which draws attention to the way in which in the past France bridged the gap between the EU North (e.g. the Ile de France) and South (e.g the Midi).

But France increasingly looks like the South, is mired in its own sense of decline and despair and no longer plays the counterweight to Germany's increasingly confident assertion of its economic power.

Kempe ends his piece with the chilling prediction:

It seems almost inevitable that the next European fireworks – and the next test of the durability of the French-German relationship – will come when financial markets turn their firepower on Paris.